The undulations of 2022 saw a hardening of the global insurance market that has had a flow-on effect right through to 2024, as businesses continue to struggle with economic factors outside of their control. With the insurance market responding to various environmental and economic factors, it’s crucial for companies and organisations to adopt proactivity in regard to risk mitigation and protection.

Hunter Broking Group is proud to deliver our 2023 market update. Understanding the factors influencing the hardened insurance market is the best way to work with the tide rather than swimming against it in today’s ultra-competitive conditions. We detail how your firm can make proactive headway to ensure you hold the best chance of accessing coverage.

Insurance Market in Review

In a bid to surpass the gravity of 2022’s natural disasters, 2023 unleashed unprecedented temperatures, exacerbating droughts, fires, cyclones, and floods. Global markets have been seriously impacted by the war in Ukraine, with the Israel-Gaza war threatening to heighten the economic volatility further. The insurance market has certainly noticed the impact of these natural disasters and global conflict.

The ongoing impacts of COVID-19 combined with the disruption of global conflict have inflated supply chain issues and costs in many industries — notably the construction sector. As Australian communities rallied to rebuild in the aftermath of extreme weather events, the heightened construction costs were certainly felt. With the cost to replace buildings higher than their insured value, an increase in the risk of severe weather events and ongoing inflationary pressure, we saw the cost of insurance premiums rise to a point where businesses were struggling to keep their policies.

As sustainability embeds itself as one of the pivotal principles of modern times, environmental accountability pressures cascade into the insurance industry. So too, does class action activity, as it increases litigation for C-suite executives across the globe. Within our own shores, there has been additional regulatory scrutiny on directors and boards and a significant influx of cyber-related crime.

If you’ve experienced a rise in premiums, faced difficulty in sourcing new policies or challenges in reviewing existing policies, you’re not alone. Increased premiums and a reduced appetite for risk are some of the fundamental characteristics of a hardening insurance market and a natural response to the cause-and-effect relationship of what is largely an unprecedented confluence of factors affecting the global insurance ecosystem.

While we’re currently experiencing a hardened market, the economic landscape began to ease in 2023, with Australian CPI inflation continuously declining since the peak of 7.8% in the December 2022 quarter. The global supply chain pressure, as shown in the figure below, grew significantly over the first year of the pandemic, reaching a record high in April 2020. It then rose to an even higher peak by December 2021. Since then, the index has come down significantly. In October 2023, it fell to 1.74 standard deviations below its historical average. With inflation and supply chain pressure easing, the insurance market should experience a flow-on effect, softening in the future.

Commercial Insurance Implications

It may go without saying that more losses experienced at the hands of extreme weather events and greater disruption to businesses caused by cyber events make more significant implications across all areas of commercial insurance.

For policy owners, premium rises are an unmistakable sign of the times. High premiums are more than insurers trying to increase profits to shareholders. Higher than-average claims coupled with ongoing higher replacement costs mean that insurers are left with little option but to increase premiums in order to continue offering coverage. However, the reinsurance market is showing signs of improvement.

Increased competition among reinsurers and ample coverage capacity saw insurance companies find more favourable terms upon renewing their reinsurance contracts on 1 April 2024. This development is set to streamline the reinsurance market for insurers, making it more manageable as they approach midyear and transition into 2025, in contrast to the hurdles encountered in recent renewal periods.

The implications of the hardened market on commercial insurance provides business owners with the opportunity to reassess business and asset values, examine cash flow efficiencies, develop a continuity plan in case disaster strikes, and implement practices and policies to solidify their operations and help protect their commercial viability in years to come. Taking a proactive stance towards risk management not only enhances your standing with insurers but also mitigates the potential fallout from adverse events, offering dual benefits.

The Insurer Response

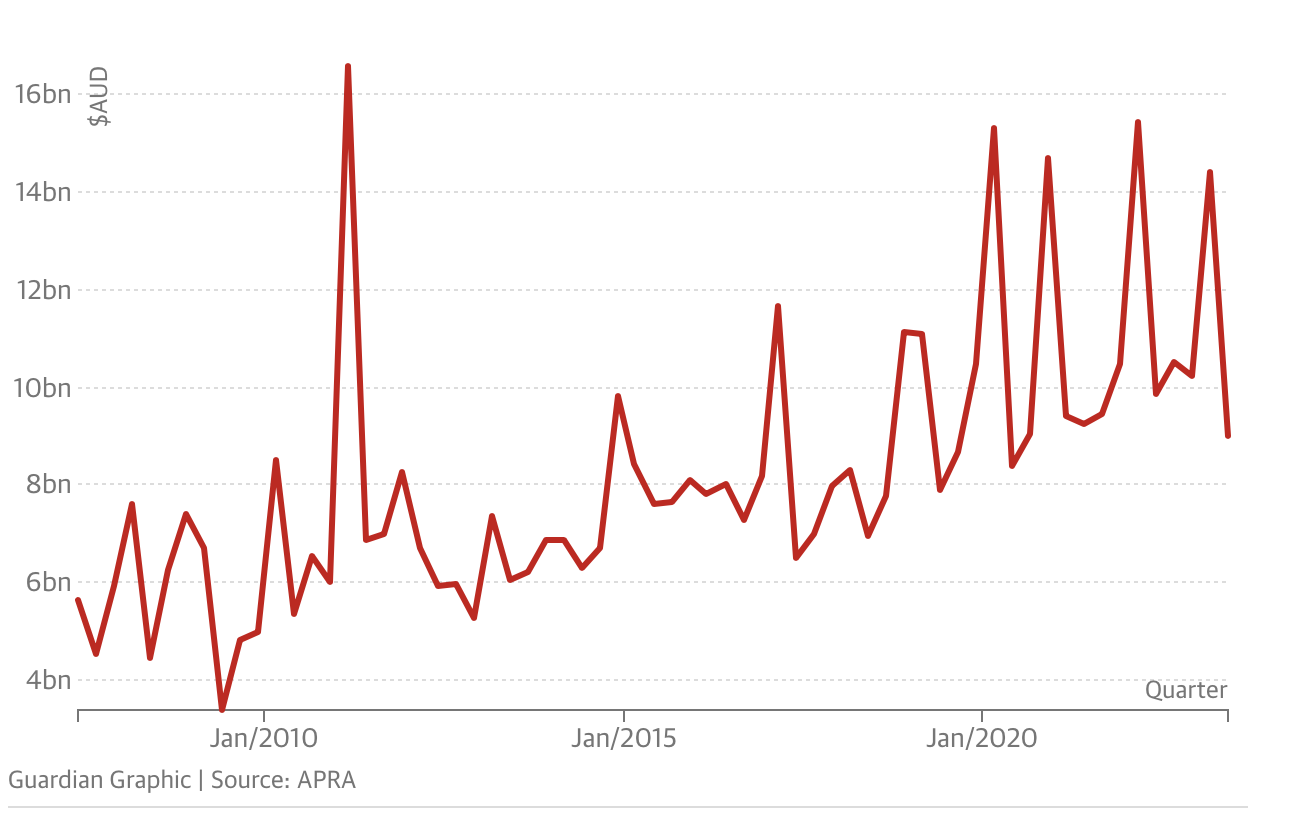

Since the destructive bushfires of 2019-20, insurers have paid out $16 billion in claims stemming from 13 declared insurance catastrophes or significant events. Past events paired with the future risk of increased events is having an ongoing influence on premiums. The below graph shows the amount of claims made to general insurers, trending in an upward direction.

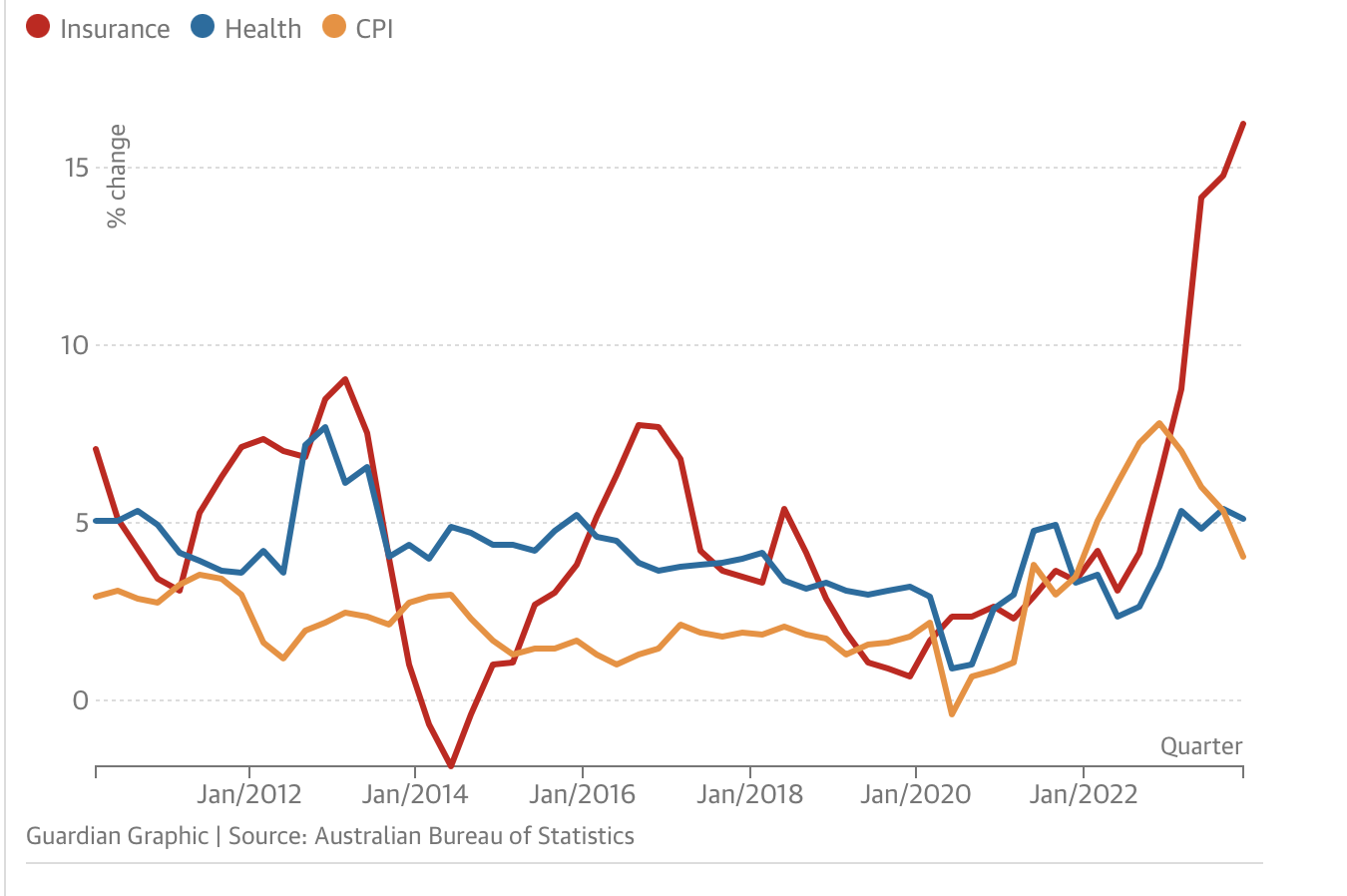

Typically, there’s a temporary surge in premiums for a year or two post-disaster, followed by a return to normalcy. However, the current landscape reflects a fundamental shift in the insurance market dynamics. Factors such as severe weather patterns and escalating costs in labour, construction materials, automotive parts, and repairs necessitate insurance premiums to rise above inflation rates. These factors and the additional layer of ongoing risk have seen insurance premiums rise significantly more than CPI.

It’s important to remember that insurance, like most things, works in cyclical markets. The actions taken by insurers are necessary to secure their operations and ability to continue providing cover in future years. Adapting to changing market conditions is certainly not a new practice for insurers and businesses alike. Understanding the objective of insurers and the factors that are influencing their ability to provide coverage can be the key to working with them, rather than battling against them, to find a solution for your firm.

The Heightened Importance of Property Risk Evaluation Surveys

For many industries, property insurance comprises a large portion of their commercial insurance needs. The tightening of the insurer belt often means that property surveys are not optional, but compulsory before policies are able to be renewed. With the present nature of the industry, insurance risk surveyors are in high demand. Renewals may be expected to be received 4-6 weeks from your renewal date, however, at Hunter Broking Group, we’re witnessing a lag in the availability of risk surveyors. Without a property survey report to present to insurers, policyholders face the very real risk of having a renewal lapse, or being declined for further cover.

More than ever, it is critical for underwriters to understand the property and business interruption exposure that exists. Inflation has a lot to answer for, with property and assets rapidly increasing in both repair and replacement value. Conversely, insurer’s capital returns decline in high inflation environments, exacerbating the gap. Business income and supply chain delays, as well as labour shortages also mean that claims have been extenuating past the adequacy of the coverage limits.

Furthermore, the sharp rise in the cost of materials, labour shortages and supply chain disruptions on top of highly inflated property and equipment values mean that without quantity surveyors, the true asset replacement cost is often seriously underestimated by business owners and policyholders. The current market is such that without a building or quantity surveyor report, your efforts to sourcing new cover or having an offer of renewal can be in vain. We strongly advocate for clients to use quantity surveyors and building surveyors to gain a better understanding of their true asset replacement cost.

Inadequate data can mean inadequate cover. Additionally, poor data quality affects the willingness of insurers to provide coverage. Property risk evaluation and quantity surveys provide a thorough and accurate profile of the property and business to be insured as well as provide transparency to the insurer on the risk management framework that exists to help mitigate loss.

By having a third-party surveyor assess both the valuation and risk of a business, it provides the business owner with timely and objective data that can then be used not only to source appropriate cover, but could also be used to leverage funding initiatives or other business ventures.

Cyber Cover Risk Management Expectations

Similar to the precondition of property risk evaluations for new or renewal cover offerings, insurers are responding to the increased prevalence of cyberattack losses by increasingly requesting evidence of a firm’s risk management culture and cyber hygiene. This can include a detailed examination of your organisation’s IT security spend, type and volume of data held, cyber strategy and governance arrangements.

Many cyber insurers want to assess how information assets are protected through security controls and the reliance on shadow IT. Working with IT organisations is not only one of the best strategies to build a formidable cyber risk management framework, but they can help firms access superior anti-virus software, implement robust IT infrastructure such as firewalls and guide business policies and procedures such as implementing mandatory password changes and using encrypted password managers.

An insurer’s risk management expectations can also extend to investigating any third-party arrangements, testing regimes, any prior data breaches and testing regimes. It is not uncommon for insurers to make regular tabletop scenarios where a condition of coverage includes the participation of senior management.

The cyber insurance market is rapidly evolving — in a bid to meet the ever-increasing demands of data privacy regulations, cyber insurers need to respond accordingly. At Hunter Broking Group, we anticipate that within the next two years, mandates will be introduced by insurers for organisations to use Multi-Factor-Authentication (MFA) before cyber-insurance coverage is offered.

Preparing for the Underwriting Process With Cybersecurity Controls

According to the Australian Signals Directorate, cyber crimes occurred at a rate of one every six minutes, costing small businesses an average of $46,000 in the 2023 financial year. Incidents surged by 23%, with the federal agency receiving 94,000 incident reports in 2022–23. With cyber-crimes increasing in frequency and significance, it’s essential to ensure your business is adequately protected.

To strengthen your cyber defences in preparation for the underwriting process, some of the top cybersecurity controls that your business can look to implement, or review, are:

- Multi-factor authentication for remote access and administrative (or privileged) controls or Privileged Access Management (PAM).

- Secured, encrypted and tested backups.

- Endpoint Detection and Response (EDR).

- Remote Desktop Protocol (RDP) mitigation.

- Web security and email filtering.

- Patch management and vulnerability management.

- Cybersecurity awareness training and phishing testing as well as cyber incident response planning and testing.

- Vendor/digital supply chain risk management.

- Logging and monitoring and network protections.

- Cyber risk improvement remains an incredibly prominent facet of commercial insurance, as it goes hand in hand with cyber insurance. Investing in Information Technology and cyber security improvement not only helps protect your business, but will be required for your business to access protection.

Why Service Matters

For C-suites, boards and business owners, our critical message is around forward planning and necessary proactivity towards commercial insurance. Rather than relying on ‘renewal reactivity’, without forward planning and prior preparation, large-scale corporations are being left uninsured, as risk tolerance of the world’s major insurers decreases, increasing competition for policies.

The selectivity and scrupulousness of insurers in the present climate is such that, without a comprehensive and convincing presentation of companies to the insurer, major global firms can be (and are) left uninsured. The benefits of accessing commercial insurance brokers are not lost on prudent Australian business owners. However, there is a marked difference in transactional brokers and those that form a relationship to understand your firm at a granular level.

At Hunter Broking Group, we pride ourselves on our relationship-centric approach to commercial insurance. With the evolution of the insurance ecosystem and the market hardening, no longer is price-hunting the favoured strategy to solve insurance price hikes.

Price chasing runs the risk of jeopardizing both your cover and service. By intimately understanding your business, we best position ourselves to work with you from a strategy perspective instead of merely facilitating the delivery of a renewal notice.

Our market guidance is to expect increases, but focus on mitigation, which takes more than shopping around for attractive quotes.

Consider partnering with an insurance broker to navigate the intricacies of insurance coverage, ensuring that you make informed decisions that align with your unique needs and circumstances. If you’d like to chat further about your business risk exposure, please do not hesitate to get in contact with us today.

(07) 3279 6592

[email protected]

Disclaimer:

The information provided by Hunter Broking Group Pty Ltd on this website is for general information purposes only, and it is not a substitute for professional advice. You should always consider the PDS/Policy wording before making a decision. Coverage may differ based on specific clauses in individual policies. Refer to the FSG on our website or by requesting a copy for our services and remuneration details.